Chapter 8:

Insurance Inspections. Do they hurt or help?

During the home insurance quoting process, the subject of inspections will come up. The inspections for insurance are not the same inspection you have done when buying the house. There are three separate inspections involved in the home insurance process in Florida. These are: inspections done by the insurance companies, a Four Point Inspection and a Wind Mitigation Inspection.

Inspections done by the insurance companies are mandatory and are done by the insurance carrier at no additional cost to the homeowner, once you bind a policy. These inspections are primarily for verification purposes. This inspection typically consists of taking measurements, photos and a visual inspection of the exterior of the home. Most times the homeowner is not even aware this inspection has taken place. Occasionally the carrier will find issues they will require the homeowner to address, such as cutting back trees, etc., or repairs that need to be made to the home. If this happens, the carrier will notify you and generally allow a reasonable time frame to accomplish the requested tasks.

As we mentioned, the two other inspections that play a significant role in homeowners insurance in Florida are the Four Point Inspection and the Wind Mitigation Inspection. The homeowner is responsible for scheduling and paying for these inspections, but they are typically less expensive if combined and completed at the same time by the same inspector. The typical price range of these inspections is between $100-$250 dollars.

The Four Point Inspection is the easier to explain and more basic of the two inspections. This can sometimes be a required inspection, depending on the age of the home. Most carriers will require this inspection to be done on homes aged 30 years or older. It covers the four highest aspects of risk to the insurance company in terms of older homes: roof, plumbing, electric and air conditioning. The Four Point Inspection gives the carrier information on the age, condition and life expectancy of these four items and helps them to determine if the home meets their underwriting requirements to be eligible for a homeowners policy with their company.

The rest of this chapter discusses the Wind Mitigation Inspections. These are not pass or fail inspections and their purpose is to identify storm protection features your home may have and what discounts you are eligible for because of these features.

The Wind Mitigation Inspection is good for five years from the date it was completed, if no changes are made to the home. However, in April 2010 the state mandated a new four-page inspection form. Inspections prior to this date are still good for the five-year period unless you are applying for a new policy or changing companies, in which case the new form must be used.

You will have to weigh the pros and cons of getting a Wind Mitigation Inspection. Inspections are not overly costly and any discount you receive due to the inspection will last the full five years. If the cost of the inspection is considerably less than the total of the discount you will receive over the five years of the inspection, it is well worth the investment of having the inspection done. Your agent can assist you in making this determination during the quoting process.

It is important to note here that you must have a current and accurate Wind Mitigation Inspection, completed by a certified and qualified inspector, in order for your agent to be able to tell you what discounts you are eligible for. Wind Mitigation Inspections can only be completed by a Certified Wind Mitigation Inspector.

All Nine Questions From the Current Wind Mitigation Inspection Form

Briefly Explained:

Here we will go over each of the questions found on the new Wind Mitigation Inspection Form, so you can get an idea of how you will do.

1. Building Code:

The year of the building code under which the home was designed and constructed. A newer code gives you the better discount on your insurance policy, due to more stringent building codes and construction methods improving over time.

2. Predominant Roof Covering:

Here the inspector will verify the permit date and date of roof installation to verify if the roof meets the minimum required building code. Currently the insurance company will apply a discount for a roof replaced since the newest building code of 2001.

**NOTE** Sections 3-9 must be accompanied by photographs. These photos must be clear and acceptable to the carrier.

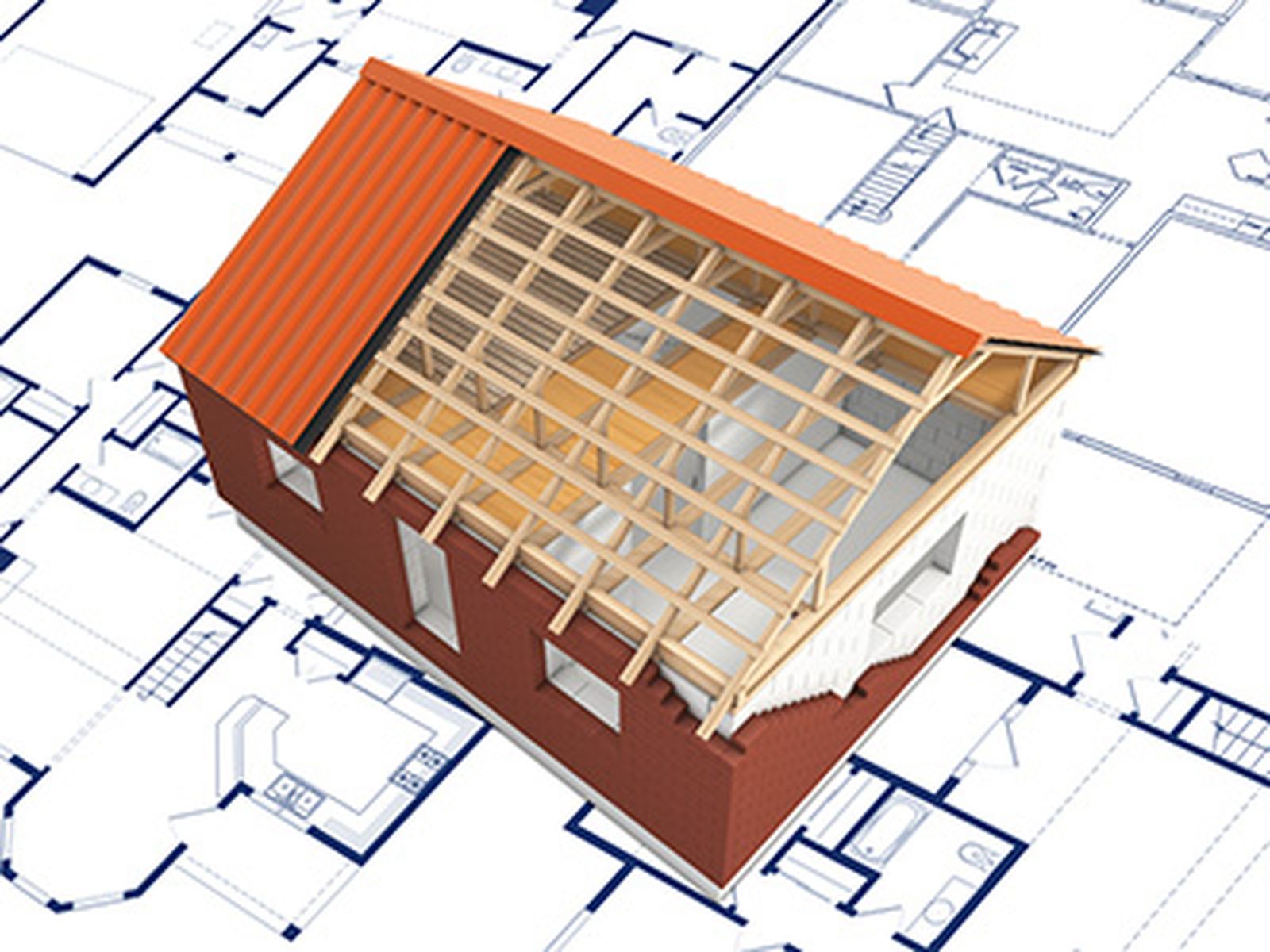

3. Roof Deck Attachment:

This section refers to the method in which the roof deck is attached to the framing. There are multiple ways the sheathing for the roof can be attached and some provide better protection in the event of a windstorm, thus giving the homeowner a greater discount.

4. Roof to Wall Attachment:

This section refers to how the roof framing is attached to the walls of your home. For the majority of roofs which use trusses, they will use the stronger attachment of what are known as Double Wraps. The weakest form of attachment are Toe Nails, where nails are used at an angle to attach the roof.

5. Roof Geometry:

There are two things to look at when it comes to the shape and geometry of your roof. Is your roof HIP shaped? A hip-shaped roof will have all sides angled down in the general shape of a pyramid, whether oblong, two that cross or square shaped. This is a common shape, but often the home is not 100% hip-shaped and in that case not eligible for this credit. Is there any flat roof, other than a carport or porch, that is not part of the roof system? Depending on how a flat roof deck or carport is attached, it can qualify the entire home as Flat Roof. A hip roof provides for the largest discount whereas a flat roof is undesirable and some insurance companies will simply not insure it.

6. Gable End Bracing:

A gable roof is a triangular roof which at times will have two or more parts that cross. The inspection here will identify the weakest form of bracing and the building code that applies.

7. Wall Construction Type:

This is a list of the exterior wall construction and the percentage of each: wood frame, un-reinforced masonry, reinforced masonry, poured concrete, or other. A concrete wall is simply stronger and less susceptible to destruction than a frame wall and would be given a better discount on your homeowners insurance policy.

8. Secondary Water Resistance (SWR):

In laymens terms, the SWR is a peel and stick material that is placed on the roof decking before the shingles are installed. If during a storm event you lose roof shingles, the SWR remains and will do exactly as the name implies: provide a secondary water resistance, which is invaluable when a roof is compromised during a storm.

9. Opening Protection:

What is the weakest form of hurricane protection installed on all exterior openings of the home? (Exterior openings include, but are not limited to: windows, doors, garage doors, skylights, etc.) To receive this discount, every opening must have verified hurricane-rated protection. There is no premium credit for plywood protection.